In this article we take a high-level look at the different ways in which prices of metal are discovered. It is intended as an introduction for those who want to develop their understanding of how commodities and metals markets work.

While the value of a particular metal can be a subjective concept – the value of a few tonnes of metal is likely to be higher to a consumer who needs it to keep their plant running than it is to someone sitting on a warehouse full of inventory – the price of a given metal at a given time can be objectively determined.

So how to go about it? Price discovery is a key function of the London Metal Exchange (LME), with the LME’s reference prices used globally for the purposes of hedging, physical settlement and contract negotiations. But across the spectrum of metals and other commodities, price discovery takes a number of different, but often interlinked, forms. Here we look at four ways prices are discovered in metals (and commodities) markets:

1. Bilateral negotiations

2. Price reporting agencies (journalistic price discovery)

3. Physical trading platforms

4. Futures exchanges

1. Bilateral negotiations

The simplest form of price discovery is a bilateral negotiation where seller A and buyer B agree on a volume of metal to change hands, now or in the future, and negotiate a mutually acceptable fixed price. This may be a one-off deal, or a recurring arrangement (the two parties may agree a regular transaction on, say, a monthly basis and negotiate a new price each time).

Bilateral negotiations have the benefit of simplicity and, because there are only two parties, lack the costs associated with intermediaries. Bilateral negotiations are typically conducted privately, which can help prevent price-sensitive information from becoming public. That said, sometimes bilaterally negotiated prices between two of the largest players are made public and used as benchmarks.

The downside of bilateral negotiation comes when one or both counterparties is managing a number of similar arrangements simultaneously, as it becomes increasingly time-consuming to negotiate multiple prices on an ongoing basis. Moreover, prices discovered during private negotiations are, by their nature, not necessarily reflective of the market as a whole – nor are they transparent.

Markets which are fairly nascent, small in size or have a concentrated number of participants (such as ferroboron and ferroniobium) tend not to have benchmark or index prices and instead are dominated by fixed-price bilateral negotiations.

2. Price reporting agencies (journalistic price discovery)

Another well-established source of pricing comes from third-party, price-reporting agency (PRA)-discovered prices. PRAs are independent companies that provide journalistic price assessments for commodities markets and the prices they discover are often used as the basis for bilateral negotiations and in the settlement of exchange-traded futures. The LME, for example, uses S&P Global Platts, Argus and Fastmarkets indices in a number of its cash-settled contracts.

PRAs use a range of methods to source prices including market participant telephone surveys and email requests, both for transactions, and bids and offers data. The data is then assessed, often using simple data calculation algorithms or using more expert judgement, depending on index and characteristics of the underlying market.

Because PRA-discovered metals prices are based on multiple market participants, they can provide a more objective and broader view of the market compared to bilateral prices. PRA price discovery is more standardised than bilaterally negotiated prices, but therefore may offer less flexibility in terms of contract customisation.

PRA-discovered metal prices are typically based on surveys that are conducted over a period of time, such as a day or a week (as opposed to real-time during futures exchange trading), which can result in a time lag between the survey and the publication of the price. This can create uncertainty in the market and limit the usefulness of the price for some participants.

While PRAs are independent from producers and consumers of metal, the prices discovered by PRAs (determined by surveys of market participants) can be subject to bias or inaccuracies based on the selection of survey participants or the methodology used to determine the price. Selective trade reporting can also be an issue.

This can limit the accuracy and reliability of the price for some market participants, although PRAs can account for variance in specification, location and grade. Also, PRAs often rely on expert judgement in their price assessments, which can introduce a degree of subjectivity into the pricing process. Despite these challenges, PRA prices are recognised as the primary reference benchmark in many commodity markets and are widely used across the industry.

3. Physical trading platforms

While PRAs source prices from participants around the market, physical trading platforms (also known as spot or tender platforms) are designed to allow those participants to transact together on a single venue.

Participants can use physical trading platforms to conclude legally binding contracts on a digital infrastructure, by inviting selected potential counterparties to submit bids or offers, as appropriate, for a volume and grade of metal.

This has the advantage of streamlining the transaction process, with the tender host in a position to assess an array of bids and offers and select the most competitive one. However, if the initial response is unacceptable the process can go through several rounds. The process can also loop back into bilateral negotiations on occasions when individual tender participants are invited to match or improve upon the best available price submitted.

Given sufficient volume, transactions concluded on the tender platform can be used to discover prices and create a price index. This method of price discovery tends to be more efficient and more representative than bilateral negotiation and PRAs. Prices are often more transparent because data points come from actual transactions and binding bids and offers.

Tender platforms also tend to allow access to more niche, less liquid markets that may not be readily tradeable on futures exchanges. They also offer more flexibility in terms of negotiation and customisation of contract terms than futures exchanges, but less so than offline bilateral negotiations.

Online tender platforms have made increasing inroads into the metals sector recently. This is partly because of the COVID-19 pandemic but also because of the efficiency and ease of handling these platforms offer amidst the ever-increasing number of data points, documents, disclosures and certifications involved in the raw materials trading process.

This has been the case particularly in non-exchange traded metals such as various ferroalloys, scrap, ores and concentrates. Metalshub, a Germany-based supply chain solution for metals trading, launched in 2017 with the aim of streamlining and digitising the physical metal trading process. As well as providing a procurement solution, Metalshub uses anonymised data from transactions to generate price indices for a number of metals. The methodology for calculating those prices and historic data is publicly available, allowing for external scrutiny.

With a view to extending this model into the base metals markets, in late 2021 the LME and Metalshub announced a collaboration agreement to improve price transparency and develop efficient digital tools for metals trading and the associated price transparency for base metals.

4. Future exchanges

The last form of price discovery we will look at is futures exchange price discovery. More specifically, price discovery based on the trading of physically settled (as opposed to PRA and/or tender-platform priced cash-settled) futures contracts. Physically settled futures contracts are contracts for the future physical delivery of a set amount of a set commodity or asset, for a set price, at a set time. In the case of the LME, delivery is made into a global warehouse network, which means prices discovered on its markets are global, rather than regional, as can be the case at other exchanges where warehouses are located regionally. It should be noted that the majority of LME contracts do not actually result in physical delivery. But it is the possibility of physical delivery, coupled with the opportunity to arbitrage any price divergence that may occur, that means prices stay in line with real-world spot prices.

This link between the futures market price of a commodity and the underlying physical market means as well that – when the market is functioning in an orderly manner – the futures prices are, in real time, reflective of global supply and demand. Futures markets also tend to attract a wider and more diverse pool of participants meaning prices discovered can be more reflective of the market as whole. Because exchanges can attract a broad range of participant types, not just physical players, this introduces differing viewpoints on price. Some participants believe these differing price views increase short-term volatility while others recognise that the increased liquidity that comes with diverse participation can actually help to dampen short-term volatility. Prices discovered on futures markets have the advantage of being transparent (based on observable trades, bids and offers). They are easily accessible, visible and are available in real-time hence removing the time lag associated with other pricing methods. Futures market pricing is based on a standardised set of specifications making for simpler transactions but removing the flexibility other pricing methods provide.

The futures market discovers not only the cash-spot price but also a forward curve up to, in the case of the LME, 10 years out depending on the metal. For major non-ferrous metals like aluminium and copper, the futures market is vastly more liquid than the underlying physical market. Futures volume of metal traded each year equates to many multiples of total annual production.

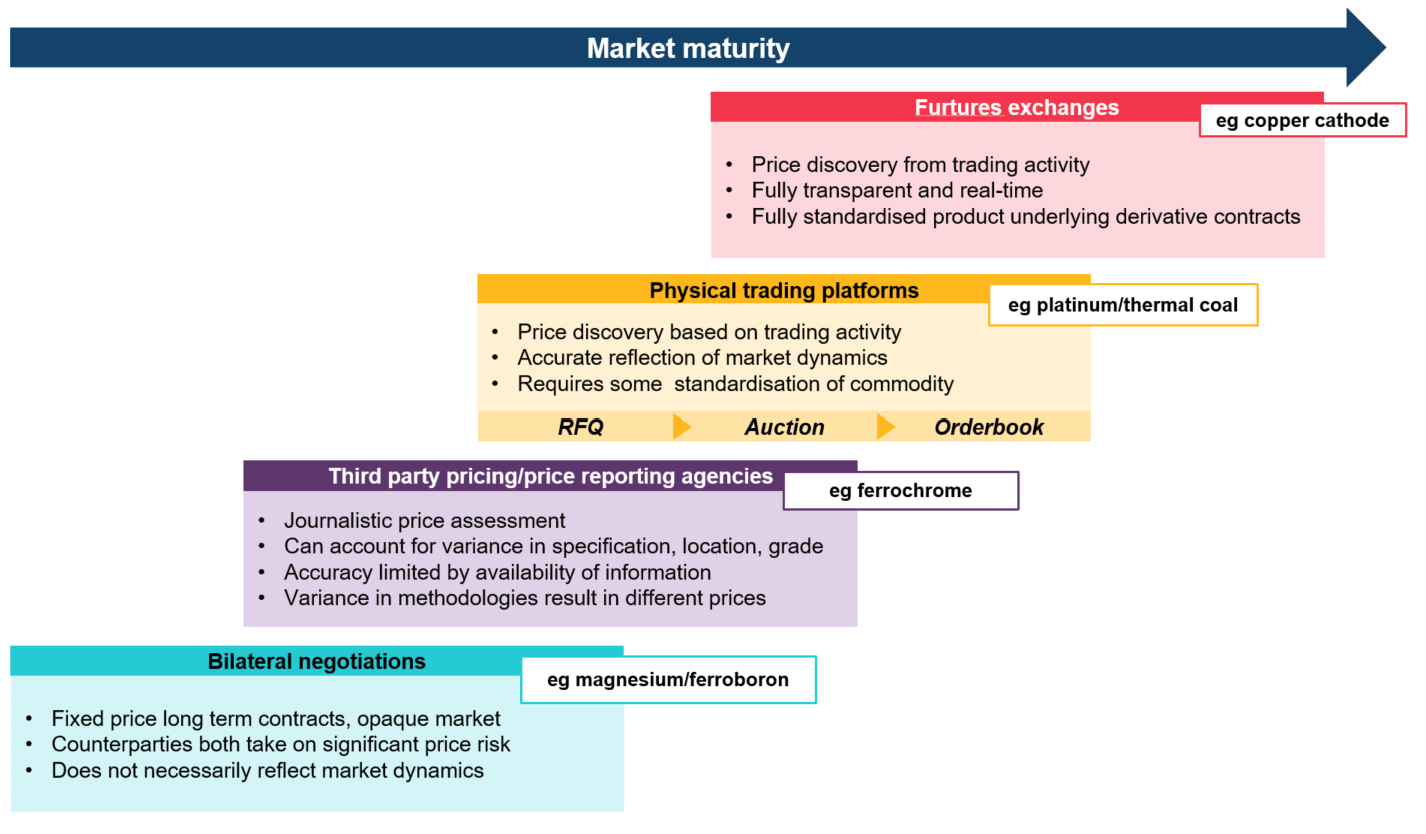

A pricing continuum

While all of these pricing methods have their unique characteristics and specific applications, it makes sense to view the price discovery process across the metals sector as a continuum, or a “maturity curve”, rather than a set of separate, unconnected activities. Each price discovery model sits at different points along this maturity curve. Highly established and liquid markets, like copper cathodes, are priced predominantly on futures exchanges, for example, while nascent markets mostly use bilaterally negotiated and/or PRA prices. Some markets sit between methods, like chrome ore, where bilateral negotiations still dominate but PRA indices also exist.

Graphic showing “maturity curve” of price discovery models

Furthermore, as markets evolve and mature, they tend to move along the maturity curve – as liquidity, transparency, the number of market participants and demand for more sophisticated hedging tools grows.

Ultimately the different price discovery methods serve different functions in the market at different stages of its evolution. The flexibility, opacity, familiarity and anonymity of bilateral negotiations are benefits to some participants and not to others. PRAs (and cash-settled futures) are suited to many, but not all, markets and they offer robust pricing in markets where physically settled futures-exchange price discovery may not be viable, like iron ore and scrap metal.

Physical trading platforms are a great tool when price discovery evolves beyond third-party pricing and the market supports more deterministic and systematic price discovery. It is also best suited for markets that do not have the scale to support exchange-based price discovery with physical delivery. For the most mature and largest markets, exchange price discovery with physical delivery is compelling given the breadth of participation, the transparent, real-time and accessible nature of the prices and robust link to underlying physical supply and demand factors.