When we read about trading in financial markets in the news it’s often the big gains and dramatic losses that make the headlines.

This can give the impression that trading is gambling, more akin to poker than to risk management. However, a large proportion of trading activity in commodities markets comes from the needs of market participants to manage their price exposure to an underlying physical product. Another factor adding to this misperception is our industry’s seemingly impenetrable jargon.

When a trader talks about carries, lending, borrowing, contango, backwardation or even kerb trading, many people simply do not understand.

In this LME Digest article, we look at the very basics of physical and financial hedging. We try to use plain English, avoiding jargon whenever possible, and explain specific terms where necessary. We are by no means attempting to provide a complete description of all aspects of hedging. Many matters, such as trade booking, accounting practices, trade clearing and trade reporting have not been included in order to focus on hedging.

Our aim is to provide a basic understanding of the interactions between the physical and financial market sides of a hedged transaction, and of the related payment obligations.

What is hedging?

When the price of metal changes it can create either a profit or a loss and affect the bottom line. Companies that make metal (producers) or companies that make things out of metal (consumers) often bear these metal price fluctuations. People commonly refer to this as metal price “exposure”. The purpose of hedging is to mitigate this price exposure and to insulate a company’s performance from market movements.

In the normal course of business, a company can see its price exposure change frequently. For example, holding additional inventory exposes a company to the risk of a financial loss if its value falls, following a drop in market prices. On the other hand, if a company agrees to future sales, at a fixed price, it exposes itself to the risk that metal input costs rise.

A company can decide to bear these risks, or take a more active approach and manage them. This “risk management” can incorporate the use of physical or financial hedges.

Physical hedging involves the pricing of bought or sold physical material to match the pricing of future production and sales. This is called “back-to-back” pricing.

Financial hedging is the action of managing price risk by using a financial derivative (like a future or an option) to offset the price movement of a related physical transaction.

Let’s take a closer look at both physical and financial hedging.

Physical and financial hedging

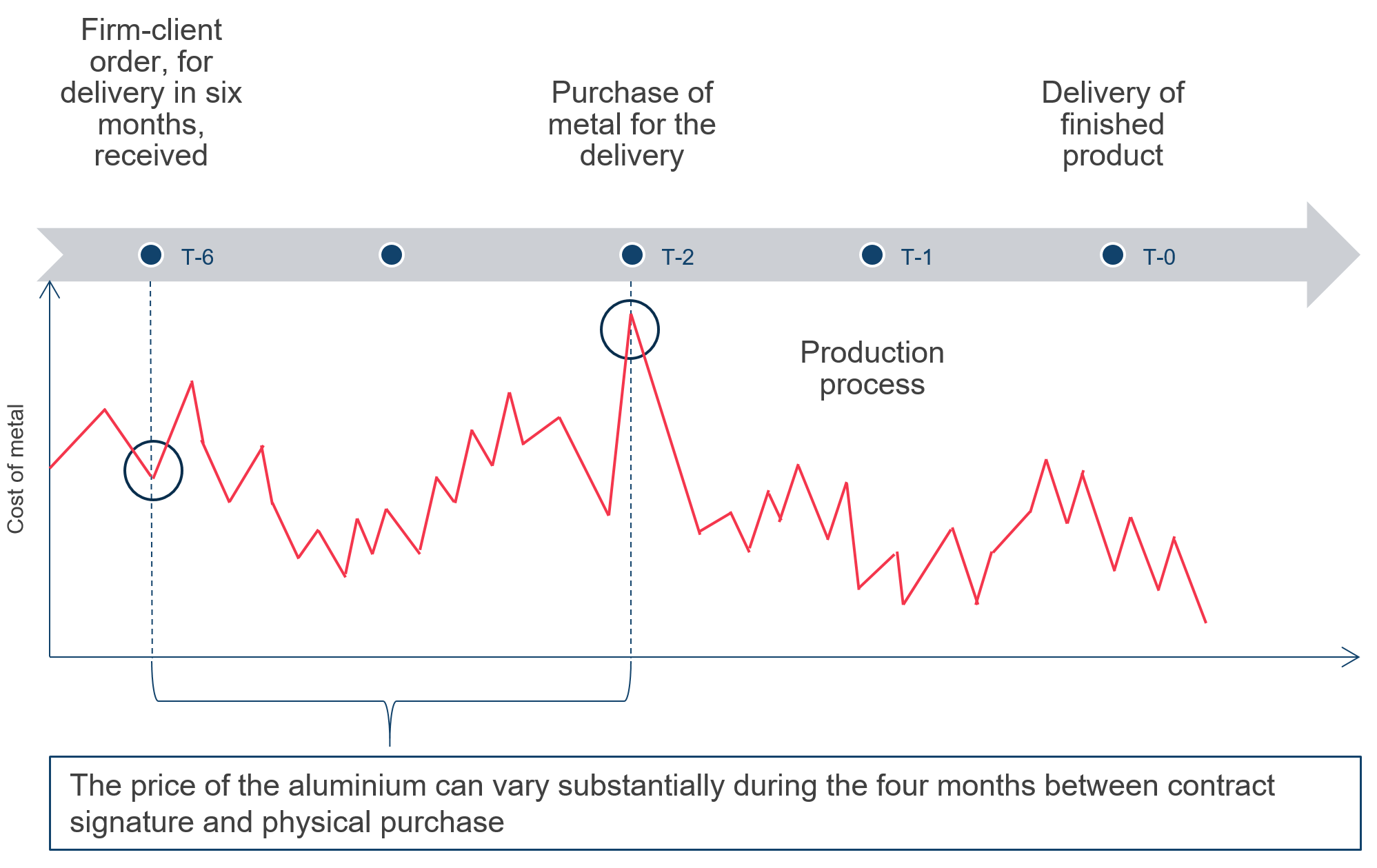

In order to secure a client order, producers and consumers of metal often need to commit to a fixed price for their finished product, for delivery in the future. Most producers and consumers aim to avoid large inventories and for that reason they will only produce the finished product closer to the delivery time. But this leaves them exposed to risk.

The price of the metal they need in order to make their finished product may rise (or fall) between the date they agreed the fixed-priced sale and the date they buy the metal. If the price of metal increases in this period, it can lead to significant losses for the company.

Let’s use the example of the fictitious aluminium equipment manufacturer, ABC Corp.

ABC Corp agrees to sell aluminium cases to XYZ Ltd, basis a fixed price of US$1900 per metric tonne (mt), for delivery in six months.

The physical hedging options for ABC Corp are:

- Buy metal in the spot market, where you take delivery almost immediately. This may not be ideal, as it leaves ABC Corp with large inventories and the associated costs of financing, storing and insuring.

- Create a fixed-price agreement with a physical aluminium supplier for delivery in the future. This may also not be the best solution as physical suppliers may charge more for assuming the price risk. Furthermore, physical fixed-price delivery agreements are subject to the risk that a supplier does not honour the agreement (performance risk) if market prices move too much in favour of ABC Corp.

In both these examples of physical hedging, ABC Corp does not bear price risk but needs to consider other issues like, as mentioned, performance risk and inventory costs.

ABC Corp could instead:

- Buy the required metal in the spot market, just before the start of production.

- Agree today with a supplier, a future delivery of metal priced at whatever the going rate is at the time of delivery – often this is basis the LME Official Settlement Price1 .

But in both scenarios ABC Corp will still have exposure to the metal price, until the metal is procured. In such a situation, financial hedging can be useful.

In our examples c) and d), the risk arises from the timing mismatch between XYZ Ltd’s fixed-price order and the time when ABC Corp procures the physical metal. The following graph illustrates this:

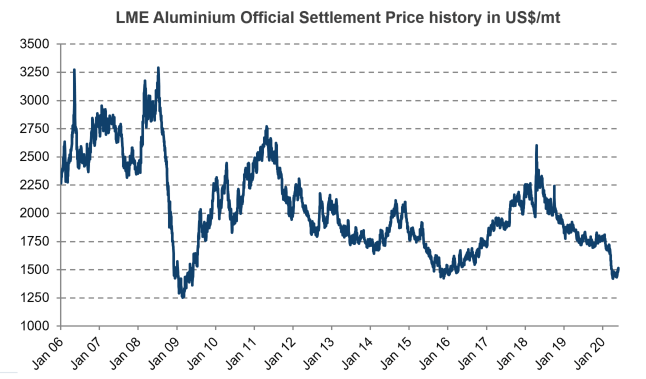

The graph below gives an idea of the magnitude of changes in the LME Aluminium Official Settlement Price since 2006:

The graph illustrates the potential risk of loss arising from such a commitment and the need to think about how to manage risk effectively. A closer look at the data confirms this picture.

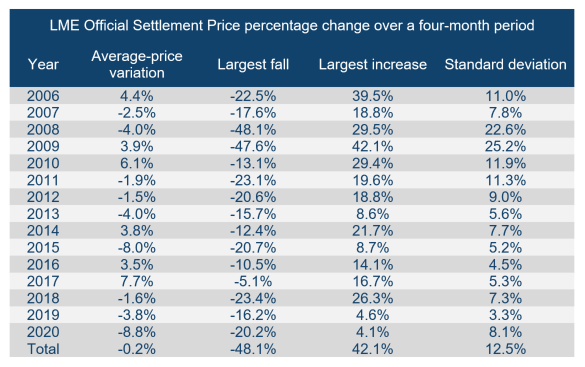

Over the last 15 years the largest price variation over a four-month (120 calendar-day) period varied between -48.1% and +42.1%. On average, the price variation over a four-month period is virtually flat at -0.2%, but the standard deviation from that number is 12.5%. This illustrates how large price movements can be.

The mechanics of financial hedging

In order to understand how financial hedging works, we need to look at both the physical transaction, where the risk originates, and the financial transaction that offsets the risk.

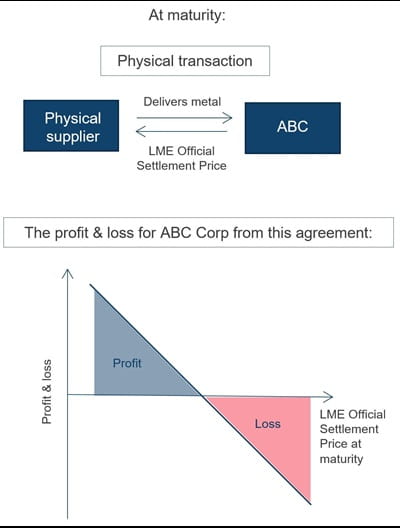

The physical transaction

ABC Corp knows that in four months (in derivatives speak, this is known as the “maturity”), it needs a quantity of metal to start production for XYZ Ltd’s order of aluminium cases. ABC Corp might purchase the required aluminium in the spot market at maturity or agree today a delivery with a metal supplier that delivers and sets the price at maturity.

The physical metal supplier will normally want to base the price of the metal on the LME Official Settlement Price.

Whether buying spot at maturity or agreeing future delivery with the supplier today, ABC Corp will pay the LME Official Settlement Price at maturity. The supplier will deliver the metal in the required form and specification. This is shown under “physical transaction” (below right). The price risk lies with ABC Corp.

If the price of aluminium goes down between the time XYZ Ltd places the order and the time ABC Corp actually buys the metal, ABC Corp will realise a gain; that is, they buy the metal at a lower price than originally anticipated.

If the price of aluminium goes up between the time XYZ Ltd places the order and the time ABC Corp actually buys the metal, ABC Corp will suffer a loss; that is, they buy the metal at a higher price than originally anticipated.

The illustration below shows how a change in the LME Aluminium Official Settlement Price affects ABC Corp’s profit and loss from the physical transaction.

ABC Corp now need to decide how to manage the situation, either by assuming the risk, or by entering into a financial hedge.

Depending on the relative importance that this metal purchase has in ABC Corp’s overall cost structure, the company may choose to hedge or to keep this risk unhedged. If an exposure is very small it may be that the company’s time and resources required to hedge outweigh the benefit.

Most companies with large metals exposure actively hedge this type of risk.

The financial hedge

We mentioned earlier that a financial hedge is a method by which price risk in a physical contract can be offset by opening a contra-position in a financial derivative. Let us now have a look at how a financial hedge using the LME Aluminium contract would work in practice.

The hedge is a purely financial agreement ABC Corp enters into via a broker, a bank or another market participant. This agreement is separate from the contract with the physical metal supplier and solely addresses the metal price risk. The hedge can be a forward, swap or futures contract. For this illustration, we use the term “financial hedge” to mean any of these instruments.

The illustration below shows how such a financial hedge works. ABC Corp agrees today to pay an agreed fixed price to the broker/bank at maturity. In return, the broker/bank will pay ABC Corp the LME Official Settlement Price at maturity. This is also commonly referred to as the “floating price” because it moves (or floats) with the market price and is unknown until maturity.

Both parties agree the fixed price when they enter the financial-hedge agreement. The floating price is determined at maturity by reference to the LME Official Settlement Price, as originally agreed.

ABC Corp in our example is thus exchanging a fixed price of US$1900 per metric tonne (mt) for a floating price. The two cash flows will net at maturity.

• If the floating price at maturity is higher than US$1900mt, ABC Corp receives the price difference.

• If the floating price at maturity is lower than US$1900mt, ABC Corp has to pay the price difference.

• If the floating price at maturity is exactly US$1900mt, nothing is paid.

The financial hedge graph illustrates how a change in the LME Aluminium price affects ABC Corp’s profit and loss from the financial hedge. The financial hedge can be bought (paying the fixed price), which protects buyers of metal against rising prices, or sold (receiving the fixed price), which protects sellers of metal against falling prices.

The instruments used for a financial hedge can serve both hedging and speculation purposes.

Financial hedging can lead to negative cash flows and should therefore align closely with a company’s broader risk-management strategy. Appropriate hedging horizons, hedging ratios and risk monitoring need to be in place. Internal stakeholders such as the commercial and procurement teams need to work hand in hand with the risk-management and treasury functions.

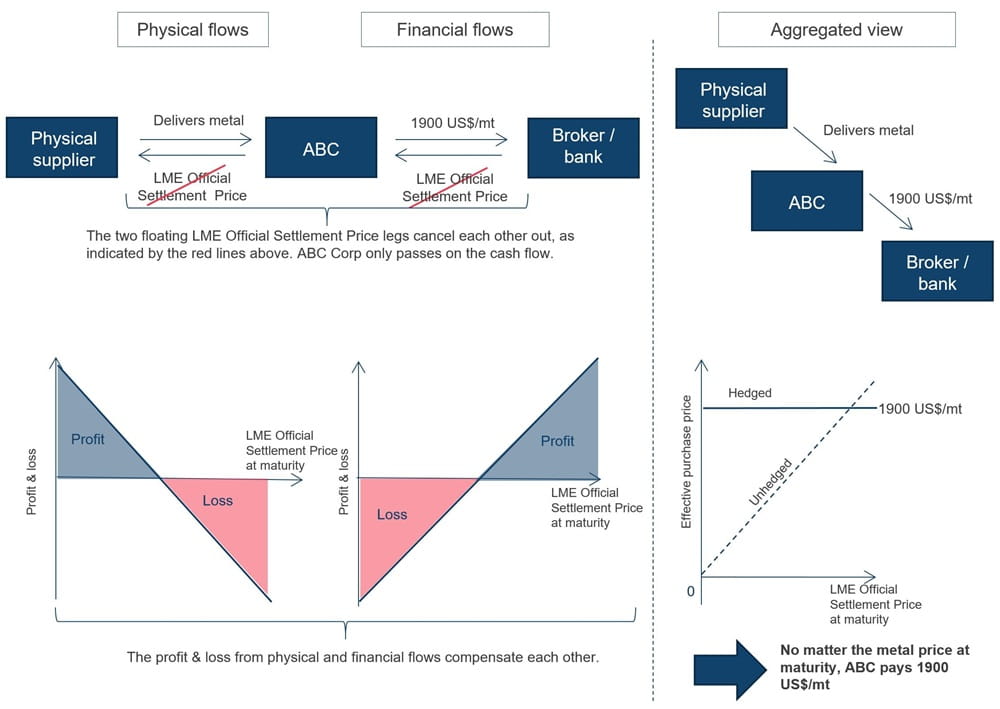

Combining the physical transaction and financial hedge - the whole picture

In order to see the big picture, we need to show the physical flows next to the financial flows. This will allow us to understand better what is happening. In the diagram below, ABC Corp receives metal at maturity basis a price that is known today: US$1900 mt.

The financial hedge converts an existing floating price profile into a fixed price.

The initial risk together with the offsetting hedge creates what is known as a “flat” or hedged position.

ABC Corp knows in advance how much the aluminium purchase is going to cost in four months time. The financial hedge fully compensates the initial physical exposure to the metal price.

The reference price

As per the example between ABC Corp and XYZ Ltd, the LME Official Settlement Price is often used as reference price in commercial contracts. Consumers and producers recognise the LME Official Settlement Price as the global benchmark, representing physical supply and demand dynamics.

The use of a reference price from another source such as a price-reporting agency (PRA) is also possible. Any reference price needs to be:

- fair

- transparent

- accessible

- accepted by the whole value chain, from producers to consumers

The reference prices used in the physical transaction and the financial hedge need to be identical or at least highly correlated. If there is a mismatch between the reference price(s) on the physical side and the one on the financial side, ABC Corp exposes itself to the risk of the two prices behaving in different ways. This risk is called "basis risk” and can affect the hedge performance negatively.

Averaging

The reference price does not need to follow a single-date observation of the LME Official Settlement Price. Many commercial agreements use the monthly average of the LME Official Settlement Price, since a single-day observation may be unrepresentative of the general price of metal over time. The LME’s Monthly Average Futures (MAFs) provide an exchange-traded solution for hedging basis monthly average prices. Bilaterally agreed over-the-counter (OTC) financial hedges can also reference monthly averages and allow for non-standard tonnage which deviates from exchange lot sizes or non-standard averaging periods, if this is required.

Separation of physical transaction and financial hedge

Some companies prefer to agree prices for future deliveries directly with their supplier - which is a valid approach.

As complexity in purchase and sales portfolios grows, the increased benefits of an active hedging approach with a separation of financial hedges from physical purchases in scenarios c) and d) become clear.

The fact that the purchase price is based on the LME Official Settlement Price means ABC Corp would often receive more comparable, competitive and transparent quotes. This is because suppliers do not need to factor in a risk buffer for assuming the aluminium price risk, which they would have needed to do if offering a fixed-price quote now.

The separation of the hedge from the physical supply agreement can also bring other advantages:

- By referencing a credible, widely accepted price, ABC Corp and the supplier can concentrate on negotiating metal specifications and delivery and packaging terms, without the need to worry about the aluminium price itself.

- It allows ABC Corp to compare offers from physical suppliers easily.

- ABC Corp does not bear the suppliers'credit risk and vice versa2.

- In combination with a financial hedge, ABC Corp also gains more pricing flexibility towards its customer XYZ Ltd and can accommodate various pricing formulas including fixed prices.

This is why many metal purchase agreements will reference the LME Official Settlement Price (and other reference prices), leaving both parties free to concentrate on providing value-added services for their clients.

Conclusion

We hope that this article helps to explain that hedging, and financial hedging in particular, is not as complicated as it may at first seem. The example of ABC Corp shows how physical transactions and financial hedge transactions work together in order to manage exposure to price risk.

Most LME members have dedicated teams who can assist you in choosing the right approach for your metal price-risk management. A list of LME members can be found here. Their experienced teams will be able to give you the information you require in order to make an informed decision.

Find out more

If you would like to find out more, please email our Head of Corporate Sales and author of this piece, Christian Mildner. You can also visit the dedicated LME education and events section on our website.

1The LME Official Price is the last bid and offer price quoted during the second session on our open-outcry trading floor, the Ring. The LME Official Settlement Price is the last cash offer price. The vast majority of physical contracts are based on the LME Official Settlement Price.

2Performance risk of the contract remains but is much easier to manage given the possibility to procure in the spot market basis the current LME Official Settlement Price.