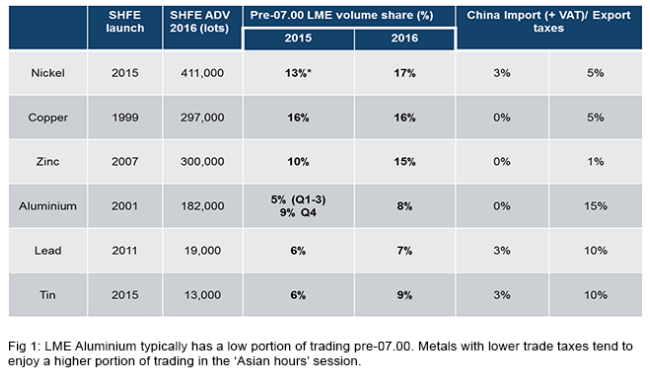

Since China imposed a 15% tax on primary aluminium exports in 2006, the Chinese and non Chinese aluminium markets have operated in relatively closed loops. China, by and large, produced its own primary aluminium, most of which remained on-shore. In turn there was little pricing interaction between LME and SHFE markets. Now the status quo appears to have changed.

A good proxy of the apparent interaction between both markets is the amount of trading volume taking place during the Shanghai day session i (pre-15.00 Shanghai/07.00 London). In well arbitraged global markets like copper, these “Asian hour” volumes on the LME and Shanghai closely correlate. Aluminium, on the other hand, is the highest-volume contract traded on the LME but has typically seen lower volumes and more stable prices than other LME base metal contracts during Asian hours, demonstrating little interaction between the two markets.

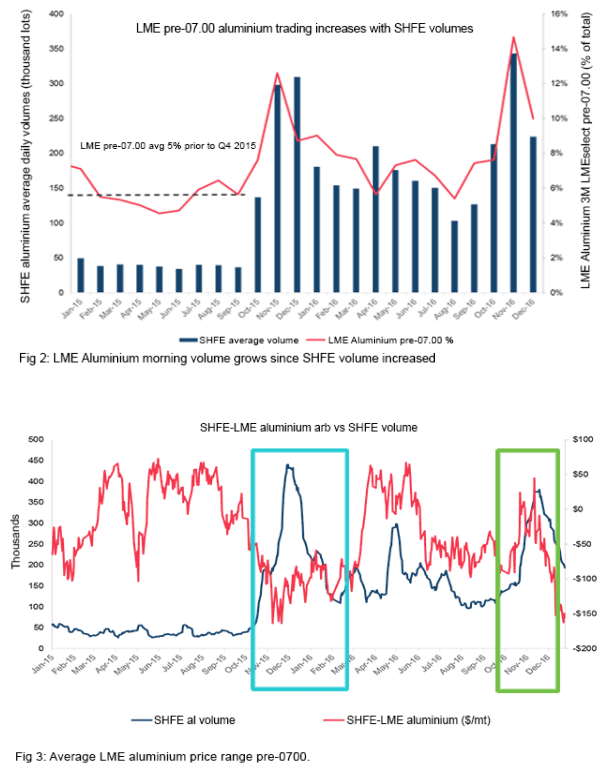

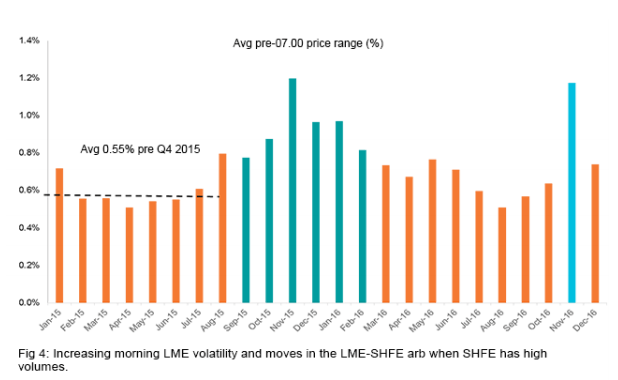

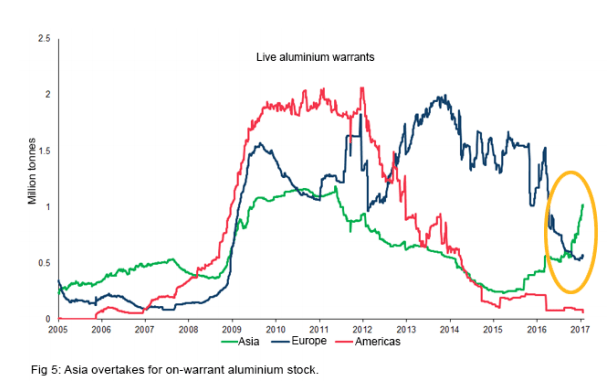

However, since SHFE volumes jumped in Q4 2015, the LME Aluminium Asian hours trading share rose to 8-9% of the total daily volume compared to 5% in Q1-3 2015 (Fig 2).The LME-SHFE aluminium arbitrage has swung more aggressively since Q4 2015 (Fig 3) and LME prices have also been more volatile in Asian hours (Fig 4). The average price range for aluminium in the London morning more than doubled to hit peaks of 1.2% in both November 2015 and November 2016, a time when Shanghai volumes were particularly high and the SHFE-LME arbitrage moved substantially.

What has driven these previously disconnected markets together?

Analysts might point to higher Chinese exports of semi-processed aluminium, which receive a rebate, making trade flows more economic. The effective ‘semi-arb’ becomes a driver for outflows of downstream materials that connect the two markets.

A genuine increase in intra-day activity suggests the relationship has widened beyond just merchants hedging physical profits. On-screen traders are increasingly trading the aluminium arb or, at least, allowing the direction of one market to influence trading on the other.

Stocks pivot East

As Shanghai gets more active, the LME Aluminium price is becoming more relevant in Asia. After the 2008 financial crisis, LME Aluminium stocks primarily grew in the US and Europe creating queues, which meant these locations held the most discounted warranted stock in the OTC markets. This presented the naturally biased location for long position holders to deliver the warrants that were picked up by the shorts, essentially shifting the LME Aluminium price to the West.

In 2016, the bias shifted back east as stocks have been steadily delivered out of western-queued locations with support from the LME warehouse reform programme. Meanwhile, tightness in the forward curve incentivises stock deliveries, which have mostly been into Asian warehouses. Crucially, on a live-warrant basis, Asia now overtakes the US and Europe for the first time since 2008 (Fig 5).

i LME calculation for trading during SHFE day time is the % of the daily volume traded pre-07.00 for the 3 month contract on LMEselect only.

ii This involves SHFE and LME prices in combination with fabrication prices/physical premia/less 13% SHFE tax rebate i.e. (LME primary aluminium + regional premiums + fabrication price) – (((SHFE primary aluminium price + domestic premiums/discounts + fabrication price) – 13% VAT rebate) + freight).