In January 2026, the London Metal Exchange (LME) implemented targeted changes to tick sizes for selected calendar spread instruments across the base metals complex. These changes were designed to enhance market quality by improving liquidity provision, strengthening price competition, and reducing inefficient trading behaviours.

Calendar spread trading plays a central role in LME markets, enabling participants to transfer risk and maintain exposure across different prompt dates. A calendar spread, or carry, involves the simultaneous purchase and sale of two contracts for the same metal with different delivery dates. These instruments are widely used by both financial and physical market participants, particularly in rolling positions forward along the forward curve. A tick size defines the minimum price increment at which a contract can trade. Historically, a uniform tick size of $0.01 encouraged marginal price improvements that allowed participants to step ahead of existing orders by economically insignificant amounts. While technically improving price, this behaviour fragmented displayed liquidity, reduced executable size at the top of the order book, and led to less reliable execution for larger trade sizes.

The revised tick size framework increases the minimum price increment for selected electronic calendar spreads, encouraging liquidity to pool at economically meaningful price levels and improving the robustness of the central order book. The changes apply exclusively to electronic trading, where larger tick sizes have been introduced to certain calendar spread contracts, alongside the existing small-tick structure remaining for other calendar spread contracts to better reflect the characteristics of different instruments along the curve. Under this framework, a large-tick calendar spread is defined as all 3rd Wednesday to 3rd Wednesday (3W–3W) and 3-month to 3rd Wednesday (3M–3W) instruments (including 3W-3M instruments) across the curve, as well as any spread where either leg extends beyond the 3M prompt – including spreads where the first leg is the 3M prompt. These large-tick calendar spreads now trade with a tick size of $0.25 for aluminium, copper, lead and zinc, and a tick size of $1.00 for tin and nickel, all small-tick calendar spreads remain at $0.01.

Analysis of the 28 trading days before and after implementation shows:

- tighter bid-ask spreads across execution sizes – up to 42% reduction for selected 5 lot trades and 23% at top of book

- greater liquidity at depth – 11% increase in how often selected 15 lot trades were available

- deeper liquidity in key month-to-month rolls (3W-3W) – with a 32-37% reduction in bid-ask spreads, with stable or improved availability for 5-15 lot execution sizes

- reduced incidence of inefficient step-ahead behaviour – concentrated but actionable liquidity.

While isolating the precise impact of market structure changes in a live environment is inherently challenging - particularly given heightened volatility linked to geopolitical developments - we deliberately analysed a 28‑trading‑day window to minimise the most acute effects of the Iran war on the data.1

Despite these constraints, the consistency of improvements observed across instruments and metrics indicates a clear positive directional effect on overall market quality. In addition to the quantitative results, participant feedback highlights a clearer and more efficient trading experience. The tick size changes have simplified price formation, reduced visual noise in the order book, and improved confidence in the availability of liquidity, particularly for larger trades.

Overall, the changes represent a meaningful step toward a more efficient, transparent, and reliable electronic market.

Market design rationale

From a market design perspective, an optimal tick size calibration must balance competing forces between price competition and liquidity provision. Research suggests that an optimal tick size is one where the average bid-ask spread is in the range of 1.5 to 5 ticks2,3,4 whilst recent WFE insights5 suggest that an instrument’s tick size should increase with asset notional value and decrease with liquidity. These findings are consistent with the LME’s new calibration across metals. If the tick size is too small, it encourages excessive undercutting, leading to queue instability and fragmented, “flickering”, liquidity. Conversely, if the tick size is too large, spreads become artificially wide, reducing competition and lowering execution probability. The optimal tick therefore lies in a middle ground, where it is large enough to discourage inefficient step-ahead behaviour and concentrate liquidity, but small enough to preserve meaningful price competition. In this way, tick size acts as a key policy lever that shapes order book equilibrium and overall market quality.

Disincentivising negative behaviour

Prior to the tick size change, participant feedback highlighted new small orders creating only marginal price improvements on existing orders in the order book, which created the appearance of low liquidity at the top of the order book. Increasing the tick size to a more economically meaningful amount aimed to reduce this behaviour - providing market participants greater certainty to execute larger orders at both the top of the order book and subsequent levels. The tick size change has pooled liquidity and avoided these negative behaviours.

LMEtrader view - trading through LMEselect

Figure 1: LMEtrader screenshot with expanded order book for AHMAR26-APR26, top of book for other spread, or carry, instruments.

Figure 1 illustrates how the larger tick size supports more meaningful price competition and visible liquidity. A greater price improvement is now required to reach the top of the book, while liquidity is more clearly concentrated at key price levels, as shown in the depth of the order book.

Tighter bid-ask spreads across execution sizes

The most significant improvements following the tick size change were observed for larger execution sizes, where both bid-ask spreads narrowed and liquidity availability increased. We evaluated this by measuring the time-weighted bid-ask spread, along with the proportion of time during which an order of a given size could be simultaneously filled on both the bid and the ask. Our analysis was generally limited to the 28 trading days following the change, reflecting a trade-off between using more data by extending the observations windows and avoiding the confounding impact of heightened market volatility associated with the escalation of the conflict in Iran in the post-implementation observation window.

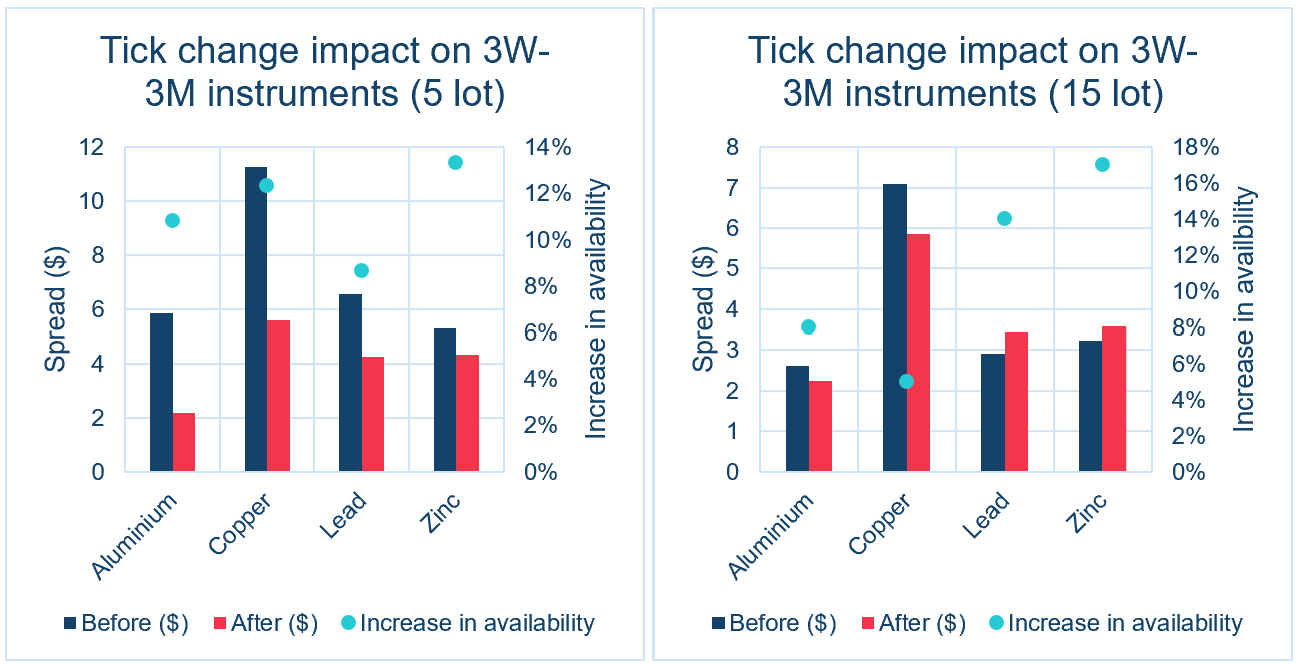

As shown on figure 2, for 5 lot executions bid-ask spreads on selected 3W-3M instruments declined by an average of 42%, while the availability of sufficient depth to complete trades increased by approximately 11%. This reflects a meaningful improvement in both execution cost and certainty. For 15 lot executions, bid-ask spreads remained broadly stable (decreasing by approximately 1%) while availability increased by 11%, indicating improved execution outcomes driven primarily by greater depth.

Figure 2: Before and after time weighted spread ($) for 5 and 15 lot execution in M1-3M, M2-3M and M3-3M, 28 trading days prior and post of tick size change on 20th January 2026. 09:00-18:00 UKT.

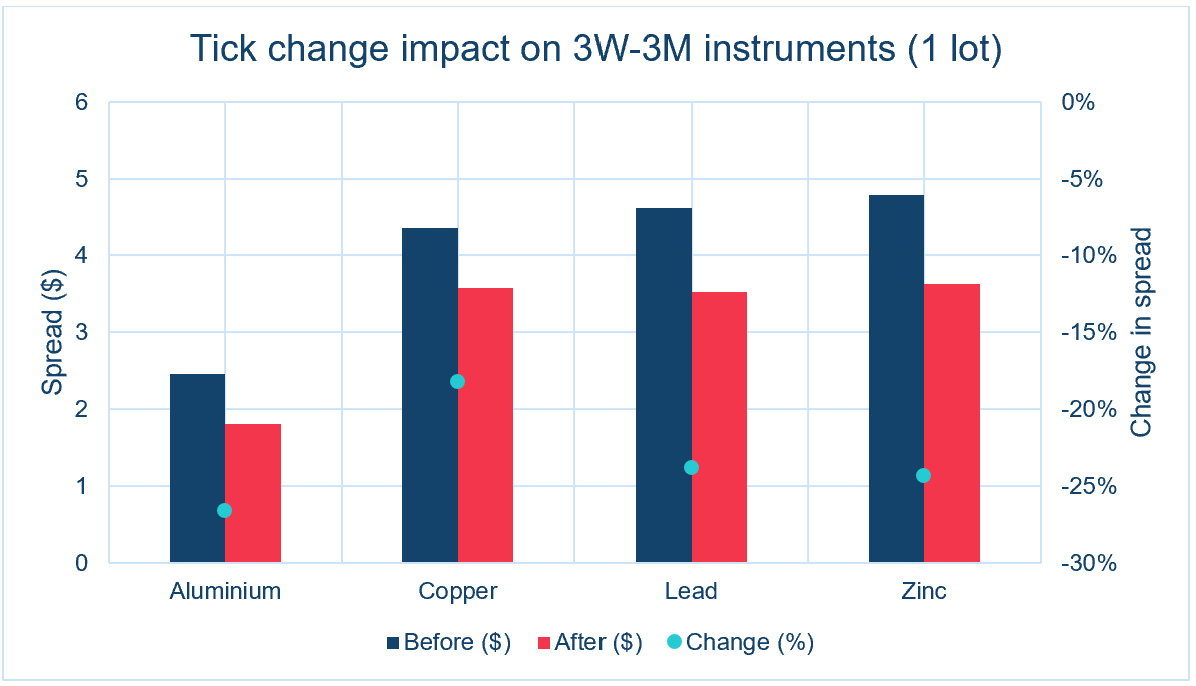

Increasing the tick size typically is associated with a wider bid ask spread at top of book, as a larger minimum price increment can mechanically widen the spread. However, as the previous tick size of $0.01 was significantly smaller than the prevailing spread it therefore did not act as a binding constraint on pricing. Across aluminium, copper, lead, and zinc, the top of book time-weighted bid-ask spread for 3W-3M spread instruments improved by an average of 23%, with aluminium exhibiting improvements of up to 27%. This represents a material reduction in transaction costs.

Figure 3: Before and after time weighted spread ($) for 1 lot execution in M1-3M, M2-3M and M3-3M. 28 trading days prior and post of tick size change on 20th January 2026. 09:00-18:00 UKT.

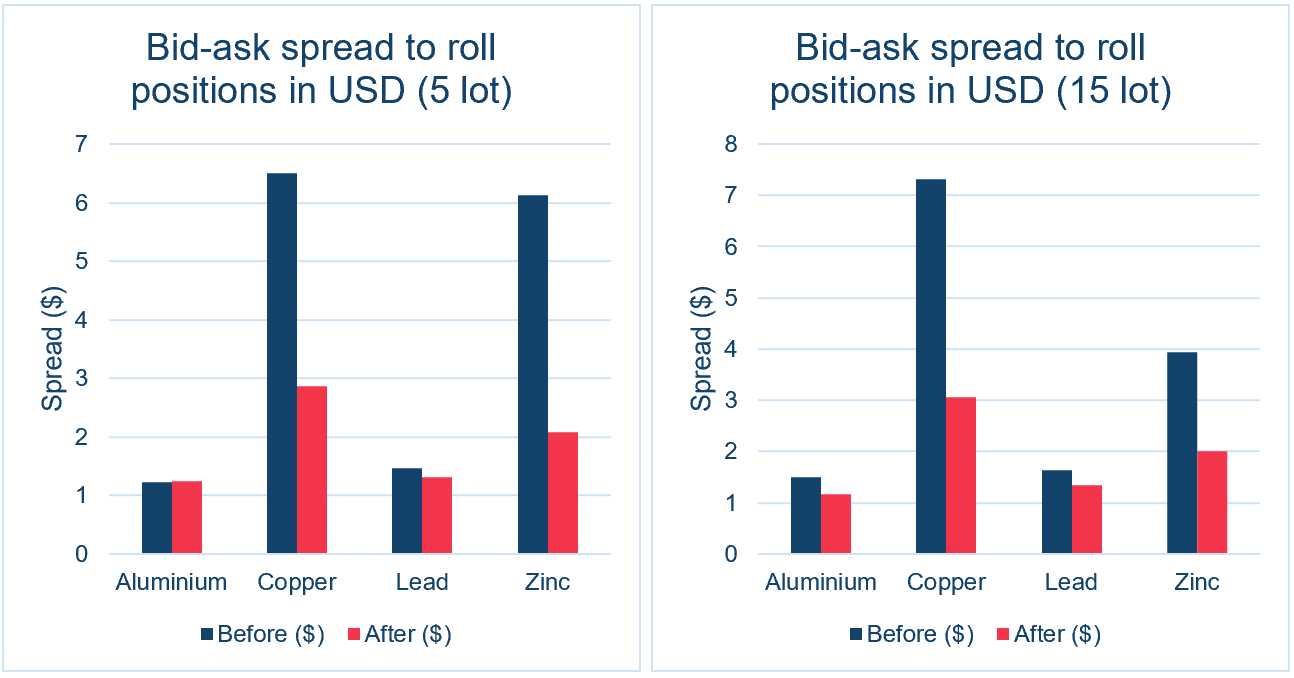

In the context of 3W-3W rolling spreads, time-weighted spreads declined by approximately 32% for 5 lots and 37% for 15 lots, while availability increased marginally. This reflects the already high liquidity in these instruments, where the primary benefit of the tick size change is tighter bid-ask spreads rather than increased depth.

Figure 4: Before and after time weighted spread ($) for 5 and 15 lot execution in M1-M2, M2-M3 and M1-M3. 28 trading days prior and post of tick size change on 20th January 2026. 09:00-18:00 UKT.

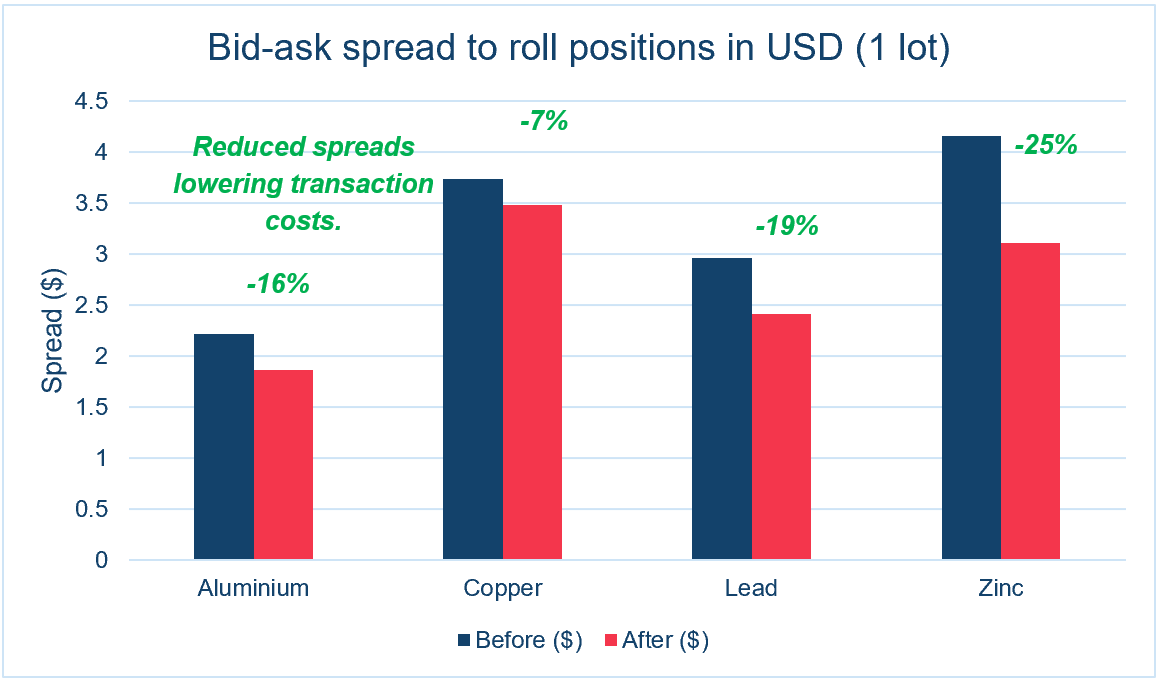

Across aluminium, copper, lead, and zinc, time-weighted bid-ask spreads for 1 lot execution on 3W-3W rolls improved by an average of 23%, with aluminium showing improvements of up to 27%, representing a material reduction in transaction costs.

Figure 5: Before and after time weighted spread ($) for 1 lot execution in M1-M2, M2-M3 and M1-M3. 28 trading days prior and post of tick size change on 20th January 2026. 09:00-18:00 UKT.

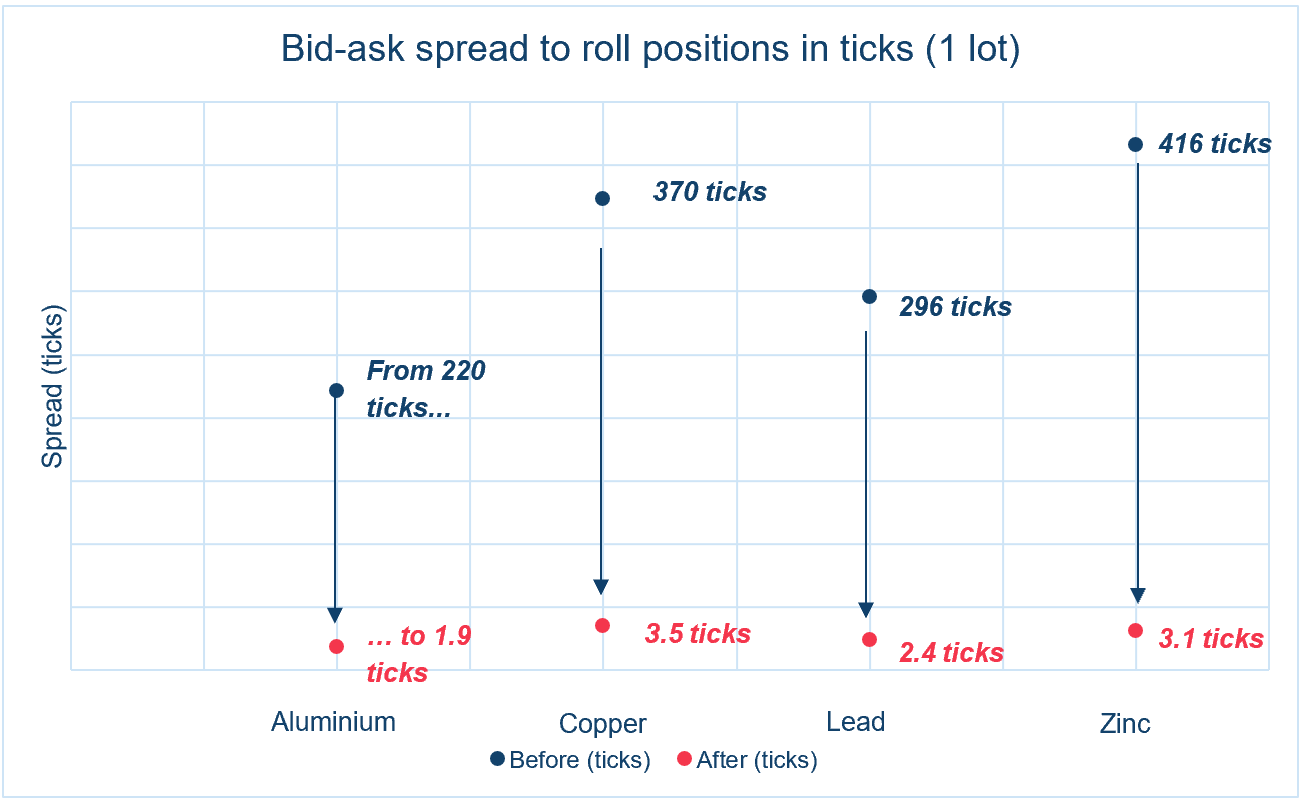

Notably, the resulting top of book spread for these 3W-3W contracts now consistently sits between 1.9 and 3.5 ticks - within the optimal 1.5 to 5 tick range often referenced in research2,3,4,5 - indicating a well-calibrated tick size that balances price competition with liquidity provision, particularly given the concurrent reduction in the spread’s dollar value.

Figure 6: Before and after time weighted spread (ticks) for 1 lot execution in M1-M2, M2-M3 and M1-M3. Event study defined as the 28 trading days prior and post of tick size change on 20th January 2026. 09:00-18:00 UKT.

More size available at depth

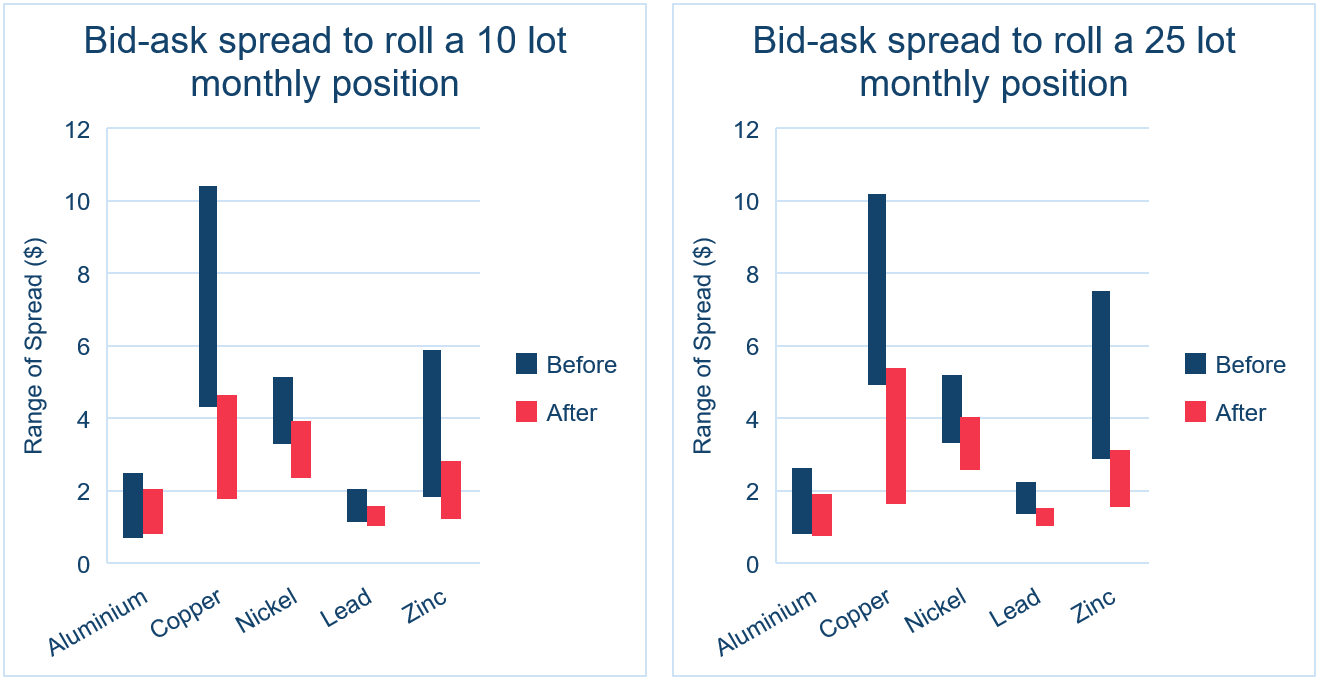

Critically, the tick size change has delivered greater liquidity at depth and increased determinism in execution outcomes. For a 25 lot execution, the time weighted spread is now lower on average across aluminium, copper, nickel, lead, and zinc, while the post change range capturing both minimum and maximum spreads is narrower and sits below the previous average, particularly for copper and zinc.

Slippage is typically defined as the difference between expected and realised execution price. Our analysis suggests a reduction in ex ante execution risk, with tighter and more stable spreads at larger sizes leading to more predictable and consistent outcomes. Similar effects are observed at 10 lot execution sizes, where both spreads and variability have declined relative to pre-change conditions.

Figure 7: Bars showing time weighted spread range ($) for 25 lot execution in M1-M2, M2-M3 and M1-M3. 28 trading days prior and post of tick size change on 20th January 2026. 09:00-18:00 UKT.

Resilient liquidity despite higher market uncertainty

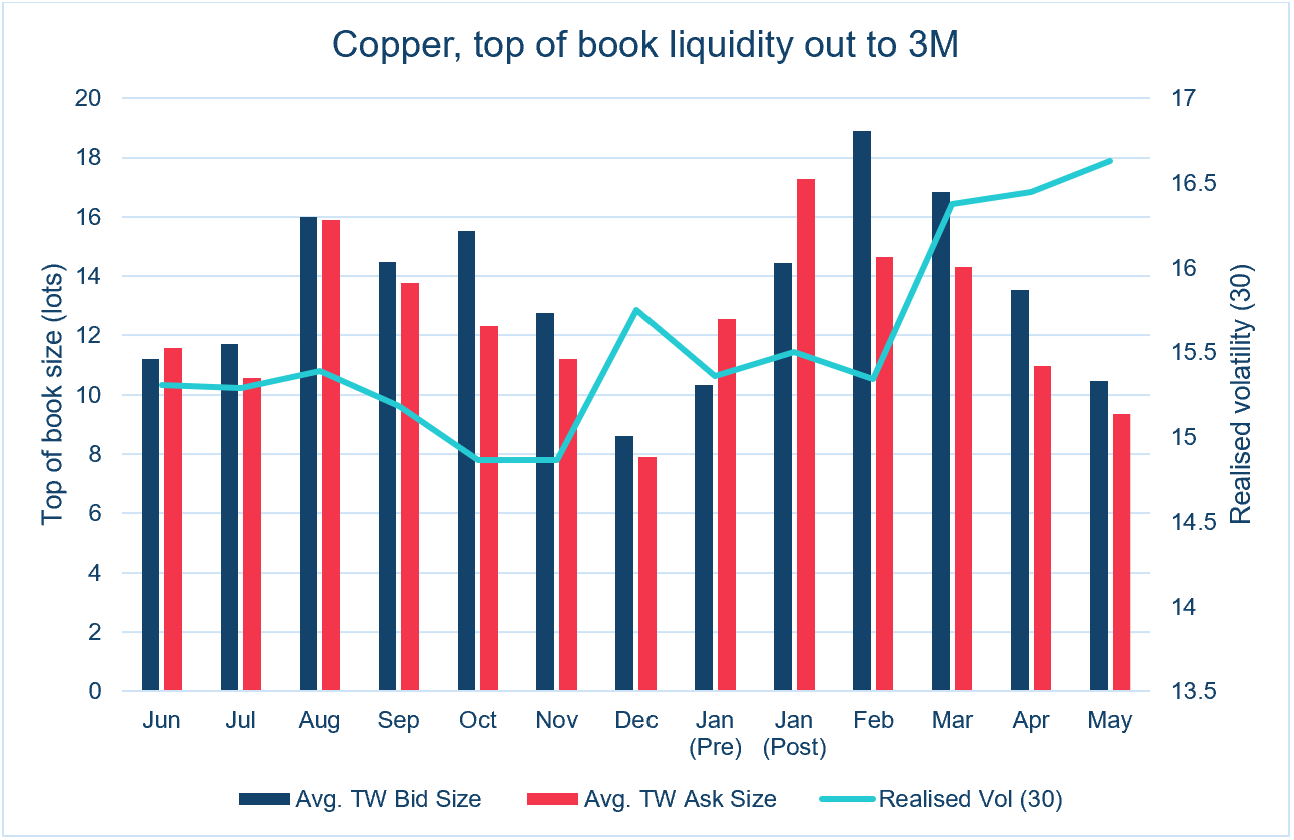

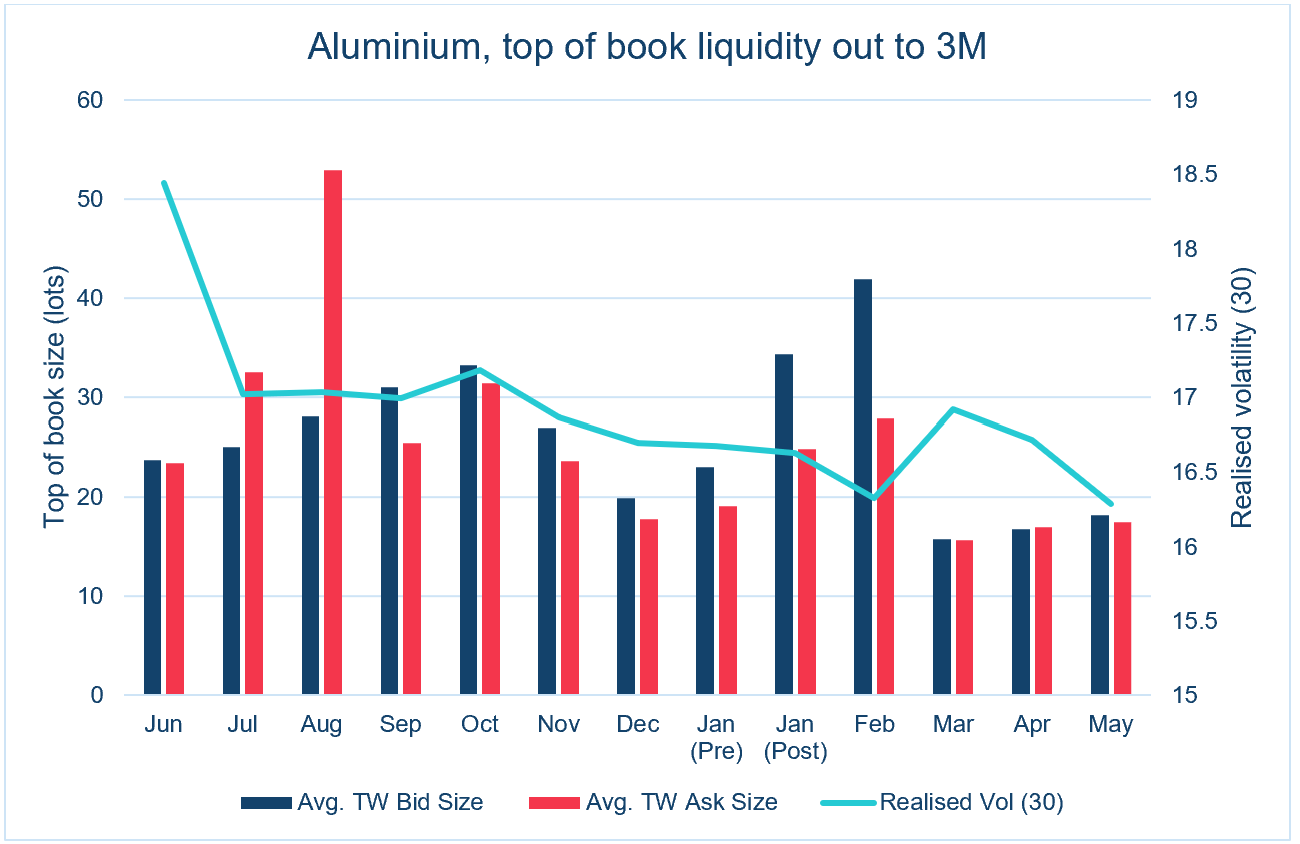

Top-of-book depth, defined as the volume available at the best bid and offer, is a key measure of liquidity. Larger tick sizes are expected to increase this depth by encouraging order aggregation.

Following the tick size change, top-of-book liquidity increased significantly across tenors for both copper and aluminium. This improvement persisted into February, even as volatility began to rise.

As volatility peaked in March, liquidity declined in line with broader market behaviour. However, post-change liquidity remained broadly above pre-change levels, indicating improved structural resilience.

While the true counterfactual cannot be observed, the persistence of stronger liquidity under more volatile conditions provides strong evidence that the tick size change improved the robustness of liquidity provision. Some divergence across metals is observed. For example, aluminium exhibited a weaker recovery in top-of-book depth following volatility spikes, suggesting that additional market-specific factors may be influencing behaviour.

Figure 8: Time weighted top of book bid and ask size for copper M1-3M, M1-M2, M2-3M, M2-M3 and M3-3M. Volatility defined as realised volatility over previous 30 days from copper data. 09:00-17:00 UKT

Figure 9: Time weighted top of book bid and ask size for aluminium M1-3M, M1-M2, M2-3M, M2-M3 and M3-3M. Volatility defined as realised volatility over previous 30 days from aluminium data. 09:00-17:00 UKT

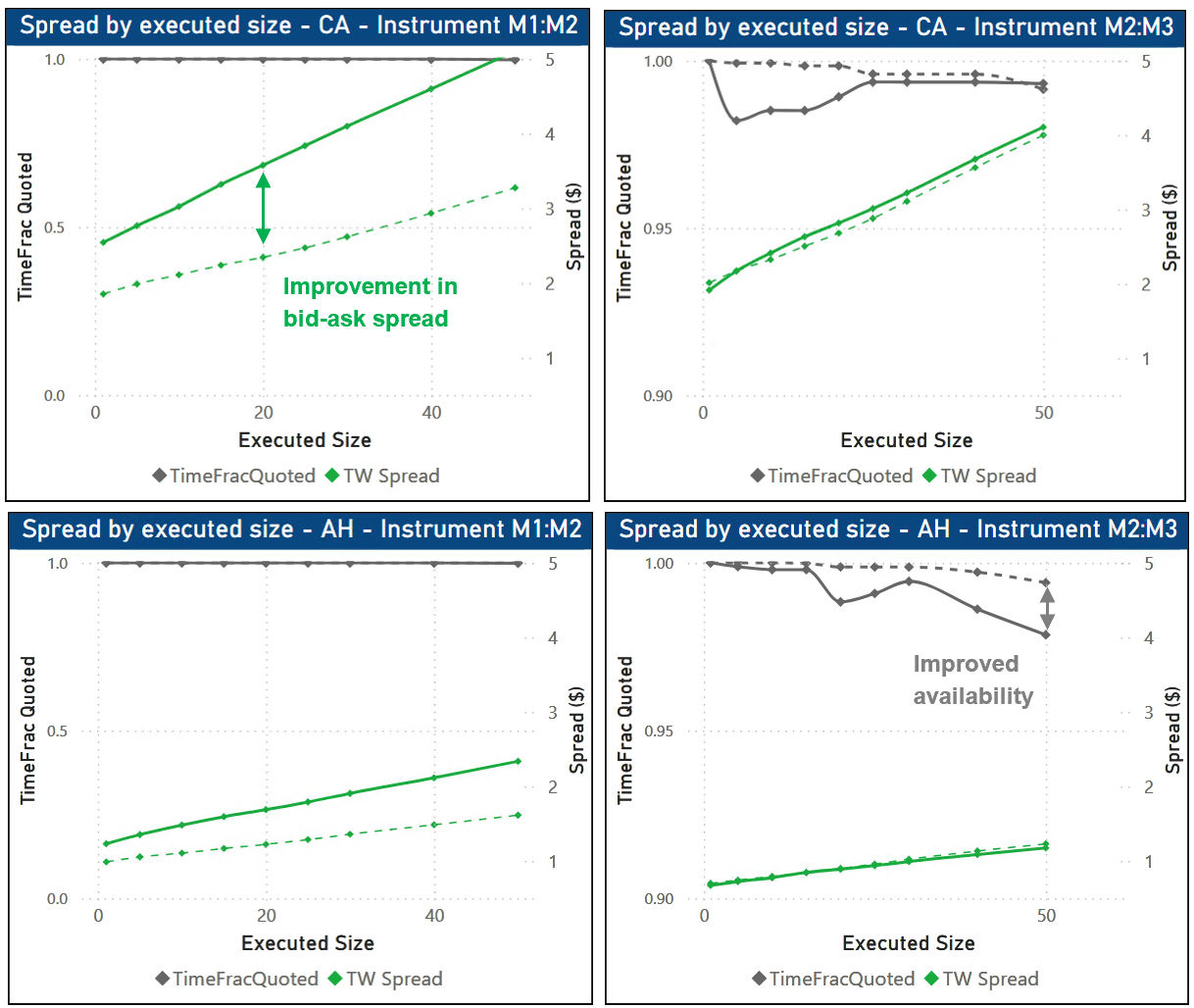

Rate of change of spread versus execution size

The figure compares the pre- and post-event relationship between bid–ask spread and execution size for aluminium and copper across the M1-M2 and M2-M3 segments. Green lines represent the time-weighted bid-ask spread, while grey lines indicate availability, measured as the percentage of time the relevant order size is quoted. Solid lines denote the pre-change period, and dashed lines denote the post-change period.

Overall, execution quality appears to have improved or remained stable. Bid-ask spreads are either tighter or unchanged, while availability is stable or has increased. For example, in the M1-M2 segment across both metals, there is a clear tightening of spreads with little change in availability. In contrast, in the M2-M3 segment, spreads remain broadly stable, while availability shows a moderate improvement.

While spreads remain largely unchanged, suggesting more reliable access to liquidity without a significant change in execution cost. In others, improvements are more pronounced with both tighter spreads and stable availability, resulting in a clear enhancement in overall execution quality.

Figure 10: Time weighted spread by executed size for M1-M2 and M2-M3 (aluminium and copper). 28 trading days prior and post of tick size change on 20th January 2026. 09:00-17:00 UKT.

Conclusion

The introduction of a differentiated tick size regime for spread instruments represents a significant enhancement to LME market structure.

By increasing the cost of marginal price improvement, the changes have reduced inefficient behaviours that previously fragmented liquidity and undermined execution quality. Liquidity is now more concentrated, visible, and reliable.

Empirical analysis indicates tighter spreads, deeper order books, lower execution costs, and greater consistency in execution outcomes. These improvements persist even during periods of elevated volatility, suggesting a more structurally robust market.

While the precise impact of the changes cannot be isolated with certainty given broader market conditions, the consistency and direction of results across metrics strongly indicate improved market quality.These enhancements form part of the LME’s broader programme to modernise market structure and support efficient, transparent, and resilient trading.

References:

1.The 28-day period preceding the event spans from 8 December 2025 to 19 December 2025, while the 28-day period following the event runs from 20 January 2026 to 26 February 2026.2. MiFID II Impact of the New Tick Size Regime.pdf

3. Research on What Ticks Make Spreads Trade Best | Nasdaq

4. A closer look at the UK tick size | FCA

5. Optimal Tick Size by Giuliano Graziani, Barbara Rindi :: SSRN presented at WFE, see: Optimal Tick Size